Have the money. When it’s time.

Post-secondary costs can vary. Use the Embark RESP Calculator to estimate what you’ll need and how your savings can grow.

Estimate Your Savings

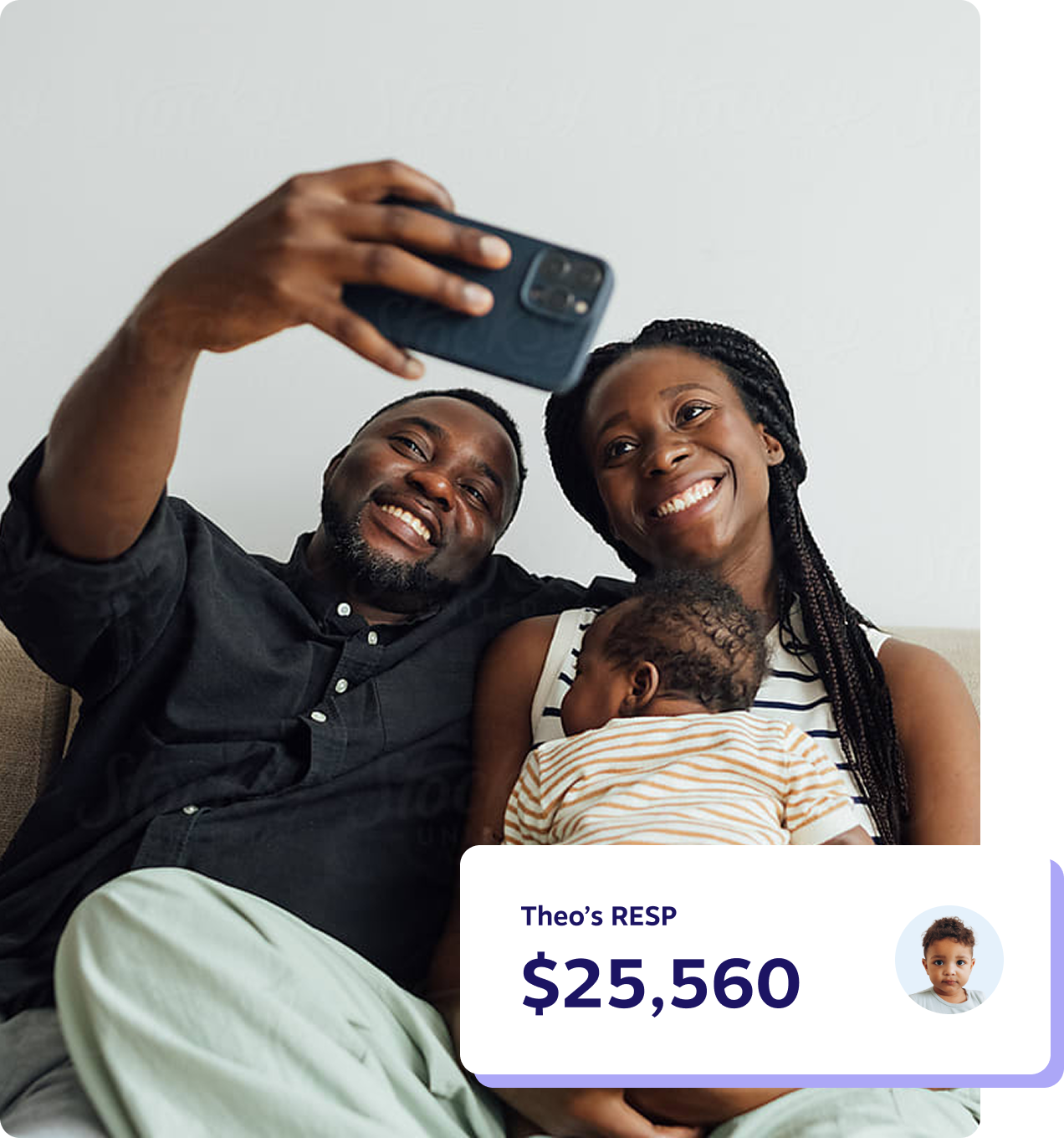

Your RESP Savings

Projected Savings

- $22,100 Contributions

- $4,420 Grants

- $8,188 Income

Average Cost of Education1

Rate of returns: 3% fixed for projection.

This projection is based on assumptions and is for illustrative purposes only. Investment returns and actual future value of your RESP cannot be predicted or guaranteed.2

Customized Guidance for You

Estimating your RESP savings is a good first step. When you open an Embark Student Plan, our savings specialists will work with you to create a custom plan that reflects the expected costs specific to your child’s education goals, maximizes government grants, and provides flexibility for the future.

Saving for the future has never been easier

- A plan that automatically adjusts to your timeline

- Simple, expert guidance helps make investing easy

- An innovative digital platform puts education savings at your fingertips

- Ability to share your plan between your children

Learn more about RESPs

To make the most of Embark’s free RESP calculator, it’s important to understand how RESPs work and how RESPs compare with other savings plans. Below, we answer all your burning questions about RESPs, like “What is an RESP?”, “What is the RESP contribution limit?”, and “How much can I save with the RESP student plan?”

What is an RESP?

An RESP, or Registered Education Savings Plan, is a registered, tax-sheltered savings account that is designed to help Canadians save for post-secondary education. More specifically, RESPs allow account holders to grow their investments on a tax-deferred basis. As long as your investment remains in the RESP account, your money will grow free from capital gains tax, interest, or dividend payments. Even better, some RESPs are eligible for federal and provincial government grants.

How do RESPs work?

When a person creates an RESP, they are the only one who can make contributions or withdrawals to and from that RESP. This person is referred to as the “subscriber.” The subscriber, who is often a parent, can open a plan for one or multiple beneficiaries, the beneficiary or beneficiaries of an RESP are usually the subscriber’s children. However, they could also be the subscriber’s grandchild, nephew, niece, or a family friend. That said, some RESPs have restrictions on who the beneficiary can be. For example, “family plan” RESPs require the beneficiary to be a blood-relative of the subscriber or related through formal adoption, such as a child, grandchild, sibling, or stepchild. No matter what type of RESP you open, the purpose of these plans is to help you save up for the cost of post-secondary education. These costs may include textbooks and equipment, tuition fees, cost of living, and more.

After opening an RESP, you will get to decide how much money to contribute to it. Unlike other registered accounts like TFSAs or RRSPs that have annual contribution limits, RESPs only have a lifetime contribution limit and that limit is $50,000 per beneficiary. Once an initial contribution has been made to your RESP, you can start investing your money. As a subscriber, you have complete control over the types of investments you choose to hold in your RESP. They may include mutual funds, GICs, stocks, bonds, or exchange traded funds, among other types of investments.

When the time comes that your beneficiary is ready for post-secondary school and is officially enrolled in an institution, you can withdraw the funds from your RESP. Payments for the beneficiary’s schooling can be made directly from these funds. Just remember that RESP funds are tax-deferred, not tax-free, which means you will need to pay tax on the amount you withdraw.

What are the advantages of an RESP?

There are a number of advantages that come with opening and contributing money to an RESP. Some of the primary benefits include:

- Tax-deferred investments: The money that an account holder contributes to an RESP is able to grow on a tax-deferred basis. Any amount that your RESP investments earn is not taxed until the money is withdrawn.

- RESP grants: The federal government of Canada and some provincial governments in the country provide grants and incentives to help increase account holders’ RESP savings. One example of this is the Canada Education Savings Grant (CESG), a program in which the federal government will match 20% of your contributions up to $2,500 per year.

- Ample flexibility: Another benefit of RESPs is that they give account holders tons of flexibility when it comes to deciding how much they want to contribute and where to invest their funds. The only restriction is the lifetime contribution limit of $50,000 per beneficiary.

- Investment options: There is no shortage of investment options when investing through an RESP. Plus, as mentioned above, there are no restrictions as to what types of investments you can invest your money in. This allows account holders to invest in everything from exchanged traded funds and mutual funds to stocks, bonds, GICs, REITs, and more.

What are the different types of RESPs?

There are three main types of RESPs in Canada: individual RESPs, family RESPs, and group RESPs. We explain each type below.

Individual RESPs

Individual RESPs allow subscribers to save money for one beneficiary’s education. They are the most basic form of RESP and are ideal for those who only have one child or who want to set up an RESP on behalf of someone they are not blood-related to, such as a family friend.

Family RESPs

Family RESPs allow subscribers to save money for one or more beneficiaries at the same time. That said, with family RESPs, the beneficiaries usually must be related to the subscriber, either by blood or formal adoption. These types of RESPs are best suited to subscribers with multiple children for whom they are looking to save.

Group RESPs

Lastly, group RESPs, which are far less popular than individual and family RESPs, are offered by a wide range of financial institutions. That said, they usually have more rules and restrictions, so it’s best to contact a group RESP provider directly to learn more about these.

What is the annual contribution limit on an RESP?

There is no annual contribution limit on an RESP. However, there is a lifetime contribution limit per beneficiary, which is $50,000.

How long can my RESP remain open?

Subscribers can contribute to RESPs for up to 31 years and an RESP can remain open for a maximum of 35 years.

Are RESP contributions tax-deductible?

No. You will not receive a tax deduction for contributing money to an RESP. That said, the money that you invest in an RESP will grow tax-deferred, so long as the money is in the RESP account. When it eventually comes time to withdraw funds from the RESP, you will be required to pay tax on the investment income earned, as well as any government grants received. However, you will not have to pay tax on the contributions you made over the years. Rather, the beneficiary or student will be taxed for these funds, but since students are usually in such a low tax bracket, it typically ends up resulting in little to no tax owing.